Business gas prices also continued to trend higher

Gas retail prices also continued to climb with the average price for 1-to-5-year contracts for medium-sized(1) businesses increasing by 30% in Q2’21 compared to the same quarter in 2020(2). The main driver is rising wholesale gas prices which during the second quarter accelerated exponentially and reached exceptional high levels for the front months and season.

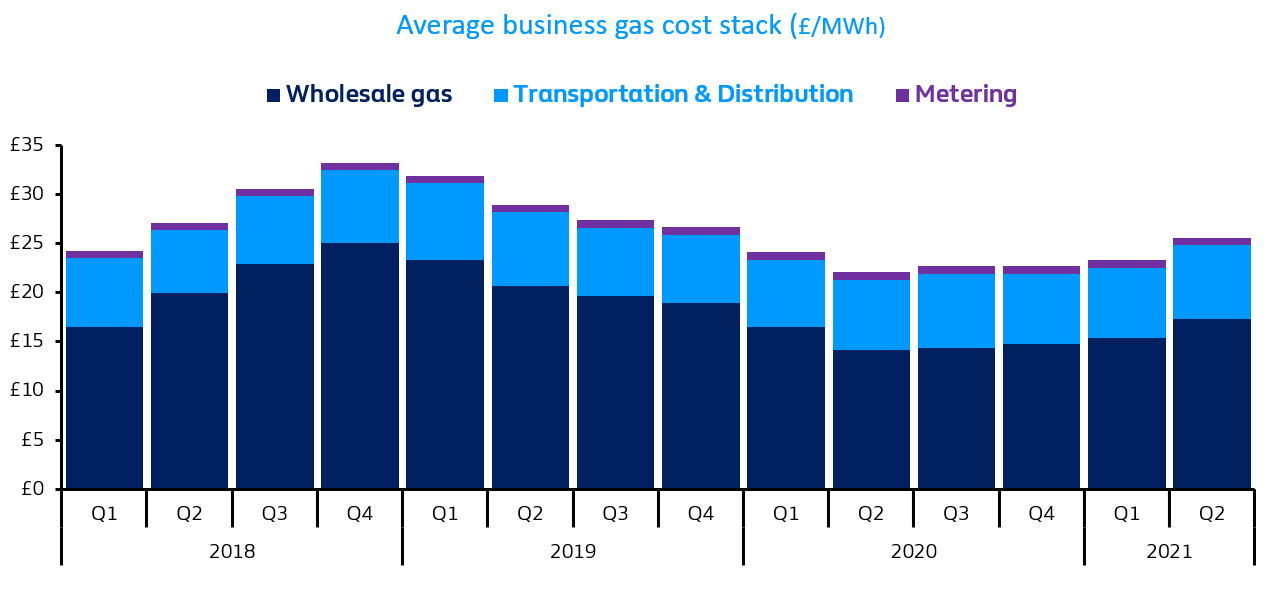

As a result, the commodity element of a typical gas bill for a mid-market company has increased for the fourth consecutive quarter and stands at 68%, that’s is 4pp higher than a year ago(5).

On the other hand, transportation & distribution charges (or non-commodity) have remained broadly stable but declined as a proportion of all costs for the third consecutive quarter to 29% from 33% in the previous three months.

Metering costs continued to account for 3% of a typical gas bill.

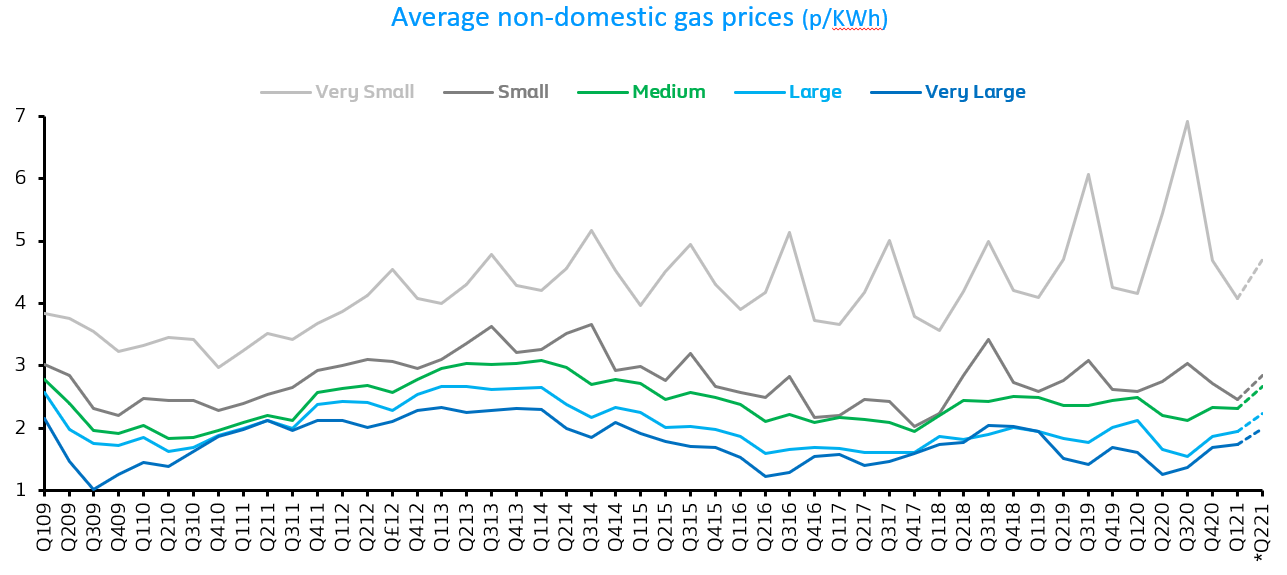

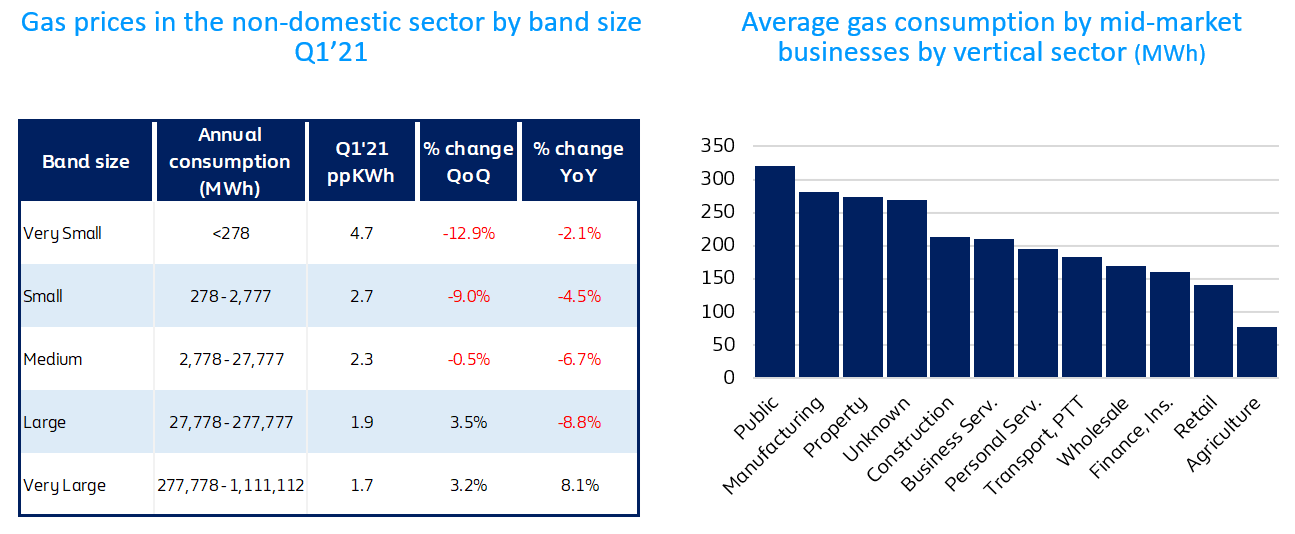

Companies of all sizes are seeing higher gas prices but the most impacted are large and very large businesses. According to BEIS’ survey of non-domestic gas prices in Q1’21(3), large and very large companies saw quarter-on-quarter increases of 3.5% and 3.2% respectively and further increases are anticipated in Q2’21 due to tight market conditions and increased demand for gas globally.

Gas price inflation in the mid-market space is likely to have a greater impact on public sector, manufacturing and property firms, which typically consume more gas on a per site basis than other sectors.

Property companies only account for 2% of all mid-sized businesses and 2% of total consumption. In contrast, retail businesses account for 41% of mid-market companies but are amongst the lowest users of gas on a per site basis(6).

Whilst gas Transportation & Distribution costs as a whole have remained broadly stable over the last three years these are starting to creep up. Local Distribution Zone capacity charges in particular are projected to increase gradually over the next five years. However, some of these would be offset by decreases in Unidentified Gas Charges as a result of a number of initiatives to minimise its impact.

Sources & Notes:

(1) For the purposes of this report, a mid-sized business is defined as an energy user consuming 150MWh and 203MWh of electricity and gas respectively per annum

(2) Based on average annualised energy prices for a mid-sized business consuming 150MWh and 203MWh of electricity and gas respectively from a sample of 18 suppliers

(3) BEIS quarterly gas and electricity prices for the non-domestic sector including the Climate Change Levy, June 2021

www.gov.uk/government/statistical-data-sets/gas-and-electricity-prices-in-the-non-domestic-sector

(*) Estimated increases in Q2’21 based on average annualised energy prices for a mid-sized business consuming 150MWh and 203MWh of electricity and gas respectively from a sample of 18 suppliers

(4) Cornwall Insight: Power prices for SME’s reach record highs, 23rd June 2021

www.cornwall-insight.com/newsroom/all-news/power-prices-for-sme-s-reach-record-highs

(5) Business electricity and gas cost stack: one-to-five-year commodity and non-commodity forecasted costs for a sample business customer with a non-half hourly meter. Non-commodity costs include: Transmission & Distribution components (TNUoS, BSUoS, DUoS) and Charges & Levies (RO, CCL, CfDs, CM)

(6) Based on modelled consumption by SIC codes using Experian dataset as of May 2021